Written by: Corey Janoff

There are plenty of guidelines out there for how to determine your retirement “number,” which is how much in total you need to accumulate in savings and investments in order to retire. Having the final target number is great, but how do you know if you are on the right track at different points in your life? Today we will look at some retirement savings targets by age to help give you some checkpoints to see if you are on track to achieving your goals.

Where to Start

In order to know if you are on track to reaching your goals, it often helps to work backwards. What is the end goal? What will you need to have ¾ the way there, half the way there, etc.? In order to get an idea of an appropriate number for the end goal, we will turn to some of those general “guidelines.”

An often-cited rule of thumb is the 4% rule, which states you can withdraw 4% of your initial portfolio balance, adjusted for inflation, and have a high probability of the money lasting at least 30 years. This has been back-tested many times under a plethora of market scenarios, and it works about 95% of the time. In fact, even a 5% withdrawal rate is safe most of the time. Obviously, there are no guarantees moving forward.

Using the 4% rule of thumb to plan for a 25-30 year retirement, you need to multiply your annual need by 25 in order to get the total amount to have at the start of retirement. 4% is one 25th of the total. A 5% rule would indicate we need 20 times our annual need. So, if you want to withdraw $100,000/year from your investments in retirement you likely need between $2 million and $2.5 million in order to retire.

If you are using today dollars to calculate your targets, we must factor inflation into the equation. Using historical average inflation, cost of living doubles every 25 years approximately. So, if you are a 40-year-old planning to retire at age 65, double the numbers in the previous paragraph to calculate what you need to shoot for at age 65. You probably need between four and five million dollars if $100k/year is your current retirement income goal at age 40.

Many Variables at Play

There are a many variables that affect how much you will need in retirement, some of them you can control and some you can’t. How much you spend, the age you retire, how long you live, income/earnings in retirement, healthcare and assisted living costs, taxes, etc. Keep that in mind as we look at numbers today. It’s not an exact science.

There are also many different ways to go about saving for retirement, as I discussed in a post in January. You could aggressively save early on and then coast in latter years. You could keep things consistent from start to finish. Maybe you are an entrepreneur and have volatile career earnings. When times are good you save a ton and in leaner years you don’t save at all. Again, many ways to approach it, but today we will look at some checkpoints to see if you are on the right track, assuming a rather consistent career and retirement savings plan.

Retirement Savings Targets by Age

In the tables below, we will use the Retirement Number on the left column as the total desired amount to have at the start of retirement. We will assume a desired retirement age of 65 for this exercise. These targets represent the collective sum (plus investment earnings) of your personal savings and any employer contributions to your workplace retirement plans.

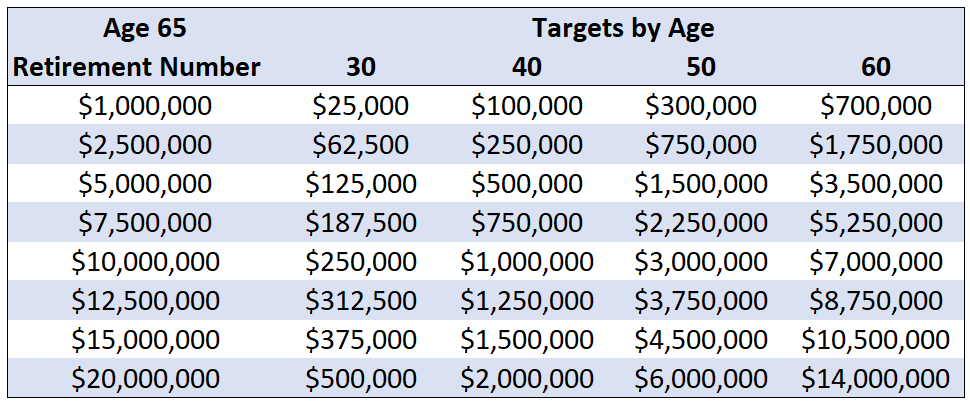

This first table will be targets for someone who is a slightly more aggressive investor in terms of risk tolerance, or someone who anticipates their earnings growth will be greater than average inflation. A common example might be a lawyer who starts their career low on the totem pole and eventually works their way up to a senior partner, earning a higher billable hour plus partnership profit distributions.

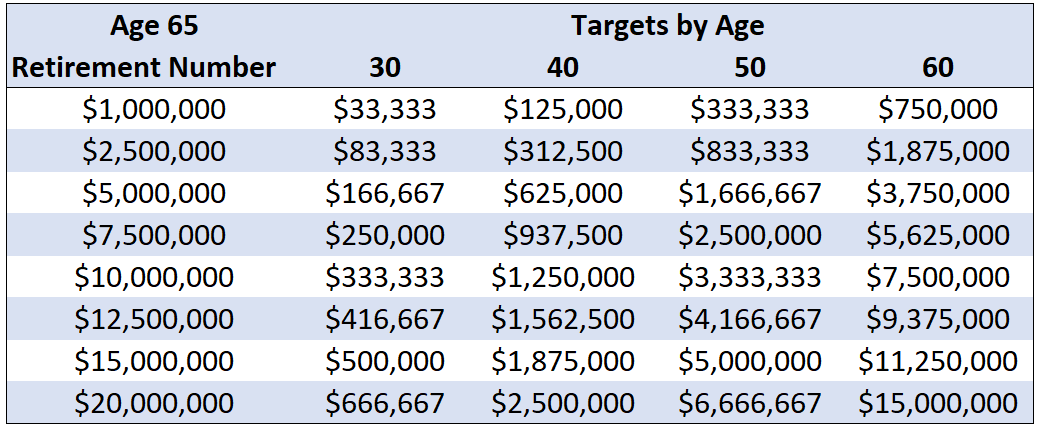

The second table consists of targets for someone who has an earnings trajectory that mirrors inflation, or maybe dials their investment risk down a little bit as they approach retirement.

If you would like to retire at age 60 instead of 65, then shift all of these targets up by five years.

If you have Social Security income, pension income, passive income from investment real estate properties, that will reduce the amount you need to draw from your investment accounts. If we use the example from earlier and target an income need of $100,000/year in today dollars, but anticipate half of your income will be covered by Social Security and other sources, then the target number you are responsible for will be halved.

Granted, there is always risk in relying on other sources out of your control. We have seen states and companies cut pension benefits before. By taking ownership of your retirement goals and ignoring income you can’t control, that will give you a higher probability of success. If you can make your retirement dreams happen without help from other sources, the rest will be icing on top of the cake.

Summary of Targets

Accumulation at the beginning stages of your career will come more from personal savings than investment earnings. If you can manage to invest a little bit in your 20’s, aiming to have 1/40th to 1/30th of your age 65 goal by age 30 is a good benchmark to shoot for.

If you are getting a late start to your career, your 30’s is the time to set the stage for future success by developing a habit of seriously investing for retirement. We typically recommend our physician clients, who don’t really start their careers until their thirties, save at least 20% of their gross income each year for retirement.

By age 40, you should probably have one tenth to one eighth of your end goal saved up. This should be the crossover point where your investment earnings begin to impact the account value more than your additions to the accounts.

At age 50, you will want to have about a third of your age 65 target number. Your 50’s is the time to really ramp up the savings. Hopefully student loans have been paid off by now. Possibly the mortgage as well. Kids may be leaving the nest in your 50’s. Some of the expenses you had earlier in your career are no longer present. Make it a priority to direct some of that free cash flow towards your retirement goals.

At age 60, you should have about two thirds to 75% of your target accounted for. Continue to invest aggressively for the home stretch. If you are ahead of schedule at this point, that could be reason to scale back on the investment risk in your portfolio, or possibly retire early! If you are behind schedule, put your head down and make a push for the finish line.

Stay the Course

In your early career, additions to your investment accounts will be the driver of the account balance increasing. As you accumulate more, investment returns will play a larger role in changes to your account balances. There will be years where your portfolios decline in value, even though you are adding significant sums to them. In those times, you must harness your inner Joel Embiid and trust the process.

In the last decade, between contributions and investment returns, there is a decent chance your account balance will double in value. That means you might only be halfway to your end goal when you are just ten years away from your desired retirement age! If you are ahead of schedule, you may be able to dial down the investment risk in your portfolio to have a smoother ride to the finish line. If you are behind schedule at that point, you may need to aggressively save or potentially revise your retirement expectations.

Use these benchmarks as guidelines, rather than mandates. Don’t get discouraged if you are behind schedule. Use it as motivation to get back on track. And don’t get too comfortable if you are ahead of schedule. Investments can be very volatile and it’s not uncommon to see a one to three year stretch of negative returns. A recession could easily change a rosy outlook (hopefully just temporarily).

You can’t control your investment returns. You can control how much you save and where you invest your money, which can give you more or less growth potential over time. The key is to keep your head down and continue to stick to your strategy over time.

Related: Retirement Planning for Doctors: How Much Do I Need to Retire?

![]()

Disclosures:

Any examples are hypothetical and for illustrative purposes only. Investments involve risk of loss, including total loss of principal. Consult with your financial advisor to develop a retirement savings strategy that suits your needs.