Written by: Corey Janoff

Health Savings Accounts (HSA’s) are a fan favorite in the financial blogosphere. According to many of the bloggers out there, the HSA is the greatest investing account known to man. It is the only triple-tax-free investment account. You can use money in it to cover healthcare expenses while you are working, and you can use the money to cover all expenses in retirement. But are HSA’s worthy of all the hype?

What is an HSA?

The Health Savings Account is a savings/investment account that can be used in conjunction with HSA eligible high-deductible health insurance plans. In order to open an HSA, you have to have a qualifying health insurance plan. That is a friendly way of saying the health insurance policy isn’t very good. The health insurance plan has to have a minimum deductible of $1,350 for an individual and $2,700 for a family and usually has a higher coinsurance payment than other health insurance plans.

For those unfamiliar, the deductible is the amount of money a person has to pay out of their own pocket before the health insurance policy will step in and start paying for medical expenses. The coinsurance is the percentage of the bill the patient still has to pay even after the deductible has been met.

For example, an individual might have a health plan with a $3,000 deductible, 30% coinsurance and a $10,000 out-of-pocket max. This means the person pays the first $3,000 of medical bills for the year and after that has been satisfied, they still have to pay 30% of all medical bills until they have spent a total of $10,000 out of their own pocket. After that point, the insurance company will pay for 100% of qualifying medical expenses (key word is qualifying).

Just because the health insurance plan has a high deductible, doesn’t mean it is necessarily eligible for an HSA. The good news is, the health insurance plans are pretty good about letting you know if it is HSA eligible.

If your health insurance plan qualifies for an HSA, you can elect to open an HSA and add up to $3,500 per year for an individual and up to $7,000 for a family. Those are pre-tax contributions, so contributing will reduce your taxable income.

Similar to a healthcare flexible spending account (FSA), the money in an HSA can be used to pay for out-of-pocket medical expenses with pre-tax dollars. The big advantage of the HSA when compared to the FSA is any unused money in an HSA will remain in the account and can be used in future years. Only $500 in an FSA is eligible to be carried over to the following year – anything above that is forfeited at the end of the year. Use it or lose it in the FSA.

Who is the HSA Most Appropriate For?

Medical expenses are outrageous in America and the cost for health insurance is just as ridiculous. However, there are many young and healthy people who have a minimal amount of medical expenses each year. They may only go to the doctor for an annual checkup and that is it. No prescriptions, no concerns. Someone in that scenario may not want to pay $500-1,000/month (or more for a family) for a top-notch health insurance plan. They might opt for a less expensive, lower-quality health insurance plan that allows for HSA contributions.

In this scenario, the individual could contribute money to the HSA so they have some money set aside just in case they do have medical expenses. Maybe they get in a car accident and have to go to the hospital. Maybe they have any number of other health issues pop up that require medical care. The money in the HSA can be used to pay for those out-of-pocket expenses.

Odds are, they won’t have any medical expenses for a handful of years, enabling them to build up a sizeable account balance within the HSA. This is ideal, because then they have the cushion to opt for an HSA eligible health plan with an even higher deductible, that would be even less expensive.

So, the HSA is ideal for the healthy person or family who can afford to cover their out of pocket medical expenses. In turn, they can afford to add money to the HSA pre-tax to be used to cover future medical bills.

What’s the Catch?

Depending on the health insurance plans available through your employer, you may not have the option to do an HSA eligible health plan. I suppose you could opt out of your health insurance at work and get an individual policy through Healthcare.gov, but if your employer subsidizes the cost of your health insurance, that would be silly. So only a limited subset of the population can even use an HSA.

As you have probably already gathered, you are taking a risk by going with a high-deductible health plan. You are exposing yourself to potentially higher out-of-pocket healthcare expenses than you would have if you went with a more expensive, lower-deductible health insurance plan.

If you can’t afford the more expensive health insurance plan and end up going with the higher deductible HSA option for financial reasons, you probably can’t afford to put any money into the HSA. In that scenario, the HSA account is useless to you. It only works if you can put money into it.

For those who can afford to contribute to the HSA, they could also afford to buy the fancier health insurance plan if they wanted to. They are most likely choosing to use the HSA as a “stealth IRA” instead.

Why is an HSA Sometimes Referred to as a “Stealth IRA?”

There are several nice things about the Health Savings Account that make it attractive to investors. For one, the contributions are made pre-tax, helping reduce taxable income. You can invest the money within the account (similar to how you invest your 401k/403b). If the investments within the account grow, all the growth is tax-deferred. You don’t owe any capital gains or income taxes on the money, as long as it stays within the account. Also, if you withdraw the money to pay for qualifying medical expenses, you can withdraw the funds tax-free. It is the only investment account where you can make pre-tax deposits and tax-free withdrawals. If you withdraw the funds for something other than healthcare expenses, you pay income taxes plus an additional 20% penalty.

Lastly, once you turn 65 years old, you can withdraw the money from the account for any reason, without penalty. You just have to pay income taxes on the withdrawals, just like your pre-tax 401k or IRA. Withdrawals for health expenses can still be made tax-free. That is how people use it as a stealth IRA. It is an additional pre-tax retirement account that can be funded at $7,000/year for a family. Pretty slick.

Final Thoughts

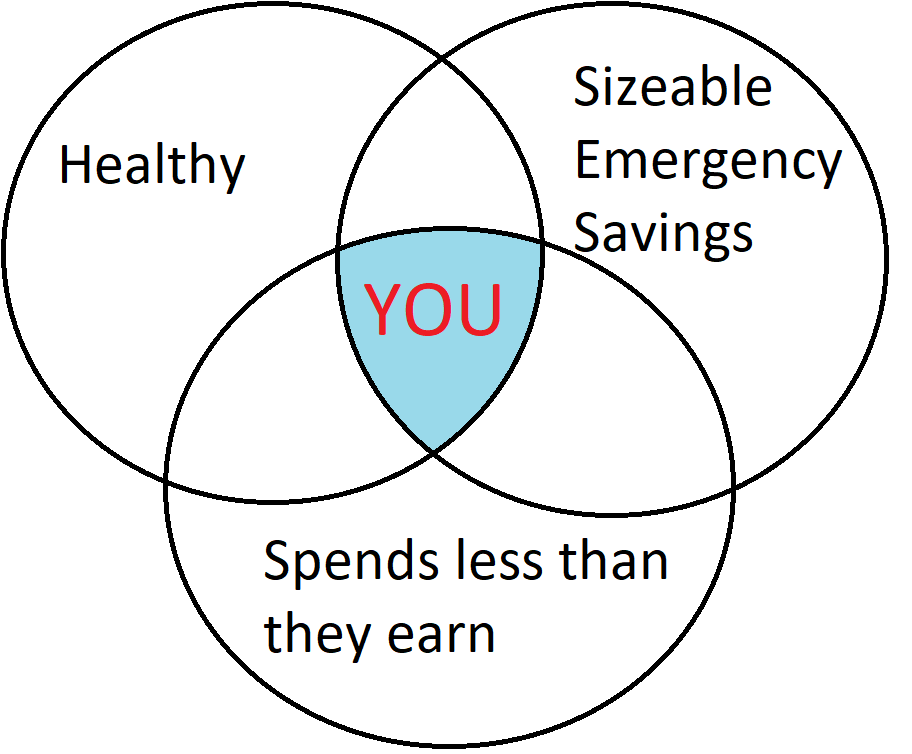

For those of you with free cash flow, who are also very healthy, who can afford to pay for out of pocket medical expenses, the HSA health insurance plans are fantastic. But each one of those variables must describe you. It’s like one of those Venn diagrams where you fall in the intersection of all the circles. If not, then the HSA plan probably isn’t appropriate for you.

If you can afford to fund an HSA, then affording out-of-pocket medical expenses probably isn’t a major concern of yours. If you can’t afford to put money into an HSA, then a high-deductible health insurance plan could be a disaster for you.

Even if you can afford the out-of-pocket medical expenses, depending on where you are in life, you may not want to take on those potential expenses. If you are starting a family or have young kids, you never know what could happen that results in expensive medical bills. You may opt for the fancier health insurance policy for peace of mind.

Finally, this might all be a moot point if your employer doesn’t offer an HSA eligible health insurance plan. Since most people get their health insurance through work, they are limited by what their employer offers. Not all employers offer an HSA eligible health insurance plan.

It would be nice if the government opened up HSA’s to everyone to be used for out-of-pocket medical expenses, regardless of what type of health insurance plan they have. They could have larger contribution limits for the traditional HSA eligible health plans and smaller contribution limit for others. But until that point, we have to work with what is available to us.

![]()