Written by: Corey Janoff

This post was originally published on our previous blog website on June 27, 2017 and has since not been revised and/or updated.

The debate between active and passive investments has rivaled the liberal-conservative clash in our country in recent years. There is no middle ground – YOU MUST PICK A SIDE! Really? Can’t we all coexist in peace and harmony? This post will take a look at active vs. passive investing and help you decide if one is actually superior to the other.

Some Background Info

For those of you that are unfamiliar with the lingo, active and passive, it is referring to how an investment portfolio (ie, mutual fund) is managed.

A mutual fund is simply a collection of a number of different securities. It could be comprised of all stocks. It could be all bonds. It could be a combination of assets.

Active mutual funds have a team of humans that make the final decisions on how a fund invests. It could be 100% based on human research and intuition. They may use a computer algorithm or rules based strategy to help make decisions. Every fund has different objectives and investment strategies, but ultimately active funds a human touch.

Passive funds, also known as index funds, attempt to remove the human influence from the equation and simply mirror a particular index. It could be a stock index, such as the S&P 500, which tracks the aggregate value of the 500 largest US companies. It could be a bond index. There are indices for international positions, commodities, real estate, etc. Some even get super specific, and try to track a particular sector of the economy, such as cyber-security companies. We are now at a point in time where there are more indices than actual stocks!

Advantages of Passive Funds

Passive funds are attractive because they are very low-cost. By mostly removing humans from the equation, they don’t have to pay all those analysts and managers with advanced degrees that active funds typically employ. They still need some people to make sure everything is running smoothly, but once the system is established, there is relatively low overhead costs to maintain it. As Benjamin Franklin once said, “A penny saved is a penny earned.”

Typically almost 100% of a passive portfolio is invested, whereas most active funds will keep at least a few percent of the total value in cash to handle fund redemptions without disrupting the overall investment strategy and placing numerous trades every day as money comes in and goes out.

Passive funds can sometimes be more tax-efficient, because their holdings don’t change very frequently, which results in less transactions and less potential for realized capital gains throughout the year. Less transactions also brings total costs down, because by trading infrequently they don’t have as much trading costs as their active counterparts typically do.

Advantages of Active Funds

Not everyone is a fan of a computer making every decision for them when it comes to their investments. Some people value having humans captaining the ship. Active funds have the ability to make adjustments in real time. If the captains of the ship forecast a storm on the horizon, they can attempt to deviate from the course they are on and try to avoid potential disaster.

Active funds have the ability to create a more customized strategy within one fund. If you are an investor that wants a combination of domestic stocks, international stocks, bonds, and commodities in your portfolio, you can find that in a single actively managed fund. Whereas you would likely need at least three or four index funds to deploy a similar strategy. If you don’t have a large amount of money to invest, or prefer a hands-off approach to reviewing your portfolio allocations, then a globally diversified active fund could be appropriate for you.

Some asset classes aren’t very transparent and have inefficiencies. Take small companies, for example. With numerous takeovers and acquisitions of small companies every year, it is hard to perfectly replicate that index. The success rate for small companies is also much smaller than the success rate of large companies. If you are investing in small companies, do you really want to take a blind, blanket approach when investing in that asset class? Or would you prefer to have a boots-on-the-ground methodology and have a team of people to thoroughly vet the companies being invested in and try to weed out the ones that don’t look very promising?

Bonds are another asset class that has some inefficiencies and can be difficult to index. Bonds are basically traded over the phone. Compared to stocks, it is quite the antiquated system. One bond dealer calls up the other and they try to strike a deal. This can make it difficult to create an index to precisely track a particular category of bonds.

So Which One is Better?

There is a reason both active and passive investments exist. Both serve a purpose and meet specific objectives.

For the average investor, passive investing is probably the way to go. It is simple, low-cost, and gets the job done. Most investors can’t tell their left shoe from their right when it comes to selecting appropriate investments to reach their goals. They don’t have the time or resources to differentiate between two actively managed funds in the same asset class.

As of late, with the stock market basically going straight up for the last eight years, passive funds have benefited the most. When a rising tide lifts all boats, the lower costs strategy will probably come out ahead.

Many proponents have climbed on the passive band-wagon recently and are bashing their active counterparts. It seems like every article or book you read on personal investing is touting index investing over active.

When it comes to investing, though, I caution anyone to merely follow the masses and media hype. There have been times in our history where active funds on average outperform passive. There have been times in history where passive funds on average outperform active. Be careful when trying to determine which one you think will perform the best in the near future.

Performance is all Relative

When you start concerning yourself too much with performance, you end up going down a rabbit hole that is hard to get out of. Performance is relative. In the late 1990’s, US stocks were doing great, averaging returns upwards of 20% per year. However, when people would receive their annual statements that showed a 20% YoY return, they were pissed! Why would someone be upset with a 20% rate of return in a year? Because their next door neighbor was making 20% per month day-trading internet stocks in his basement!

Internet companies skewed everyone’s perspective of what was considered good performance. Publically traded companies literally would add “.com” to their company name and would see their stock price go up 75% in a matter of days. Why invest in a diversified portfolio when you can double your money in a few weeks by investing in internet stocks?

We all know what happened next. Most of those companies turned out to be worthless, went bankrupt, and investors lost tons of money. The people who quit their day jobs to trade internet stocks in the late 90’s are the same people who quit their day jobs and began flipping houses in the mid-2000’s. The end result was similar.

Investor Behavior and Asset Allocation Matter Most

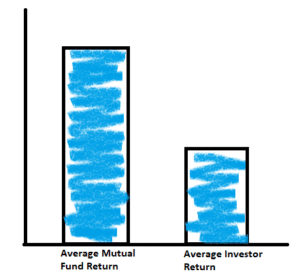

Investors are often their own worst enemies when it comes to managing their investment portfolios. Investment Research company, DALBAR Inc, publishes a study every year about how the average investor performs relative to the mutual funds they invest in. Every year the results are pretty similar. Over time, investors realize about half of the total returns that the investments themselves generate. So if the average mutual fund that invests in stocks generated a 9% annualized average rate of return over the last 20 years, the average investor only realized about 4.5% per year. This is primarily due to buying and selling at inopportune times. Rather than investing money and leaving it invested, people try to time the market and move in and out portfolios and invest in whatever did the best recently.

DALBAR Inc., also recently completed a study to try to determine whether active or passive investors perform better over time. Their conclusion: there is no clear winner. Recently, passive seems to have the upper hand, but over a longer time period, active fund investors seemed to fare a little better.

The often cited Brinson-Beebower study that researched what factors contribute to investment portfolio performance determined that over 90% of a portfolio’s returns are derived from the asset classes held in the portfolio. So over a long period of time, it really doesn’t matter whether you own Apple or Microsoft stock, Coke or Pepsi stock, an active small company mutual fund or a passive small company mutual fund. What matters most in determining portfolio returns is whether you invested in large company stocks in general, small company stocks, international stocks, bonds, or all of the above.

Mutual fund giant, Vanguard, who is famous for pioneering the index fund and advocating low-cost investing, also recognizes the power of quality professional financial advice. They have completed, and periodically update, a study they call Advisor’s Alpha. Their study determines that investors who work closely with a financial advisor can benefit significantly over time compared to investors that invest without professional guidance. This is due to financial planning, behavioral coaching, portfolio rebalancing, tax minimization strategies, and portfolio construction. Behavioral coaching is the biggest contributor to investor success – helping clients to make appropriate investment decisions when it matters most. So whether you are using active or passive investments, it can pay to have professional assistance.

It’s All About Reaching Your Goals

There are numerous other studies out there that research variables that can be attributed to financial success. I’m sure more will come in the future as well. One thing that I believe is conclusive is investors who set goals, develop a plan to reach those goals, and stick to the plan will likely see better results than someone who doesn’t do those things. Regardless of whether active or passive funds are used in the investment portfolio.

Whenever I have an initial phone conversation with a prospective client, I always ask them about their financial and life goals. What are you hoping to accomplish in life? What are you hoping to gain from working with me? What goals do you have? When would you like the ability to retire? What do you want retirement to look like? Do you want to pay for your children to go to college? Do you plan to support your parents in the future?

People can have many different goals. Some say they want to be able to retire by 60. Others want to support a charity or social cause they believe in. Some want to be able to take one big international vacation every year. I spoke with one guy recently who wants to be able to take a 6-12 month hiatus mid-career.

A goal I have never heard from a client in those initial phone calls is: “I want my investments to outperform the S&P 500 index.” Or, “I want my investments to outperform my brother’s investments.”

All that really matters is that you are able to reach your goals. If you are able to pay for your kids to go to college, you aren’t going to be sitting in the audience on graduation day, waiting for your son or daughter to walk across the stage, wondering what the annualized investment return of the college savings account was. You will be elated that your son or daughter is about to graduate college and you were able to afford the tuition! You will be equally as elated that you don’t have any more tuition to pay for! Unless grad school is in the plan…

If you are able to successfully retire one day, you aren’t going to look at your retirement portfolios and ask yourself if your investments beat their respective benchmarks during your career. All that you care about is you are able to afford life in retirement! Life is good! You made it! Time to party!

Speaking of benchmarks, the only benchmark you should have for your investments is the one that matters most, which is: Are you on track to reaching your goal? If you aren’t on track, what needs to be done to get back on course (hint: invest more)? If you are on track, pat yourself on the back and keep on plugging away.

Disclosure:

These are the opinions of Corey Janoff and do not necessarily reflect those of Finity Group, LLC or Cambridge Investment Research, Inc. Any examples are hypothetical and for illustrative purposes. This is not to be construed as individualized financial or investment advice. Be sure to consult with your financial advisor and review a fund’s prospectus before investing in a particular fund.

![]()